PromptPay is one of the reasons daily payments in Thailand feel so fast once you have a local banking setup. The Bank of Thailand describes PromptPay as payment infrastructure that makes transactions easier, faster and lower-fee. In everyday life, that translates into instant transfers by phone number or ID, QR payments at shops and markets, and a habit of asking, “Can I scan?” instead of handing over cash.

For visitors and new expats, the important detail is that PromptPay is not just an app you download for a holiday. It is connected to Thai bank accounts and participating financial institutions. If you have a Thai bank account and mobile banking, PromptPay can become central to daily spending. If you are a short-stay tourist without local banking access, you will still use cash, cards and travel wallets more often.

What PromptPay Does

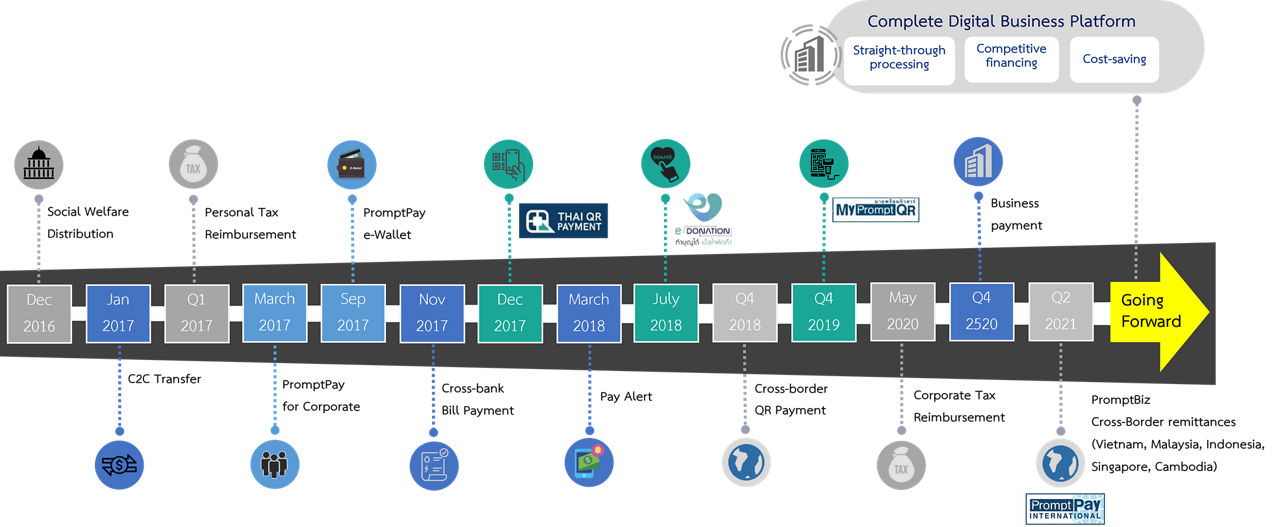

The Bank of Thailand says PromptPay lets users transfer money through digital channels using citizen ID, mobile phone number, other recipient identification numbers or bank account number. It launched in 2016 and has expanded beyond simple transfers into services such as social welfare distribution, C2C transfers, tax reimbursement, corporate PromptPay, e-wallet links, cross-bank bill payment, Thai QR payment, Pay Alert, e-Donation, cross-border QR payment and MyPromptQR.

That list sounds technical, but the reader-useful point is simple: PromptPay is infrastructure behind a lot of Thailand’s low-friction digital payment behaviour. When a food stall, cafe, taxi driver or small shop shows a Thai QR code, the payment may be riding on this ecosystem.

Fees And Limits

BOT’s PromptPay page includes a standard fee table. It lists transfers not exceeding THB 5,000 as free; more than THB 5,000 to THB 30,000 as under THB 2; more than THB 30,000 to THB 100,000 as under THB 5; and more than THB 100,000 up to the bank maximum limit as under THB 10. BOT also notes that since 2018 most banks have waived fees for digital payment transactions such as mobile payment.

For most daily spending, the practical result is that PromptPay feels free or nearly free. Still, your bank’s app, account type and transaction limit matter, especially for larger transfers, business use or cross-border functions.

How Registration Works

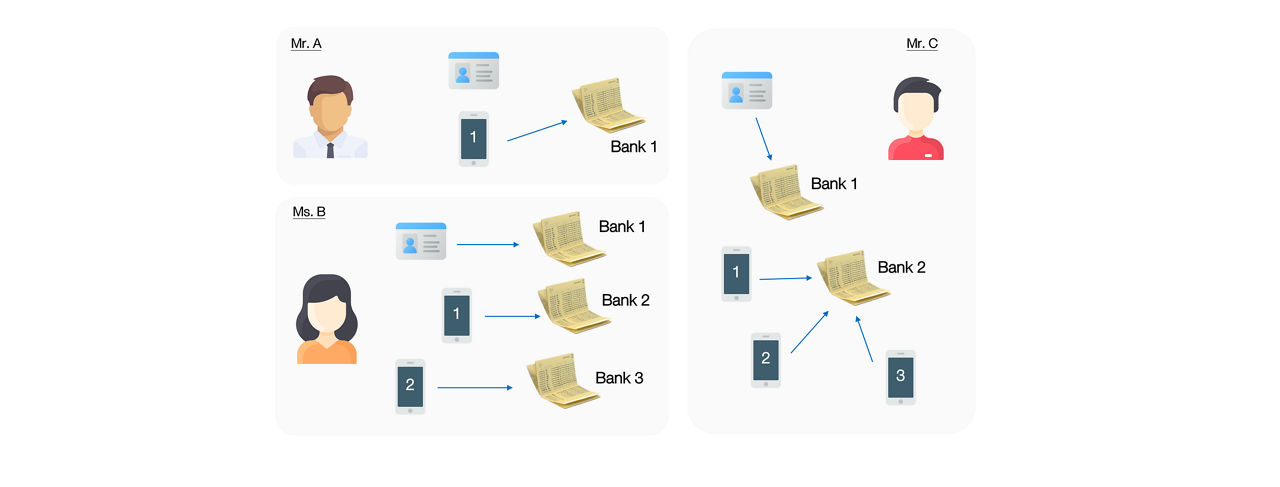

BOT says users can register by linking an existing bank account with a citizen ID or phone number through channels such as mobile banking, internet banking, ATM machines or branches. One useful detail from BOT: individuals with accounts across different banks do not need to register PromptPay for every account. They can choose one account for receiving money via PromptPay, or link different identifiers to different accounts.

For foreigners, the exact options depend on bank policy, account type and documents. A Thai mobile number and a local account make life easier, but eligibility and app flows vary. Do not assume a tourist eSIM and overseas card will give you full PromptPay capability.

How Visitors Should Use This Knowledge

If you are visiting Thailand for a week, PromptPay mainly matters because you will see QR codes everywhere. You should still carry cash for small stalls, transport gaps, islands, markets, temple areas and moments when cards fail. If you are staying longer and opening a Thai bank account, ask the bank how PromptPay registration works for your account and whether your mobile number can be linked.

If you are paying by QR, always check the merchant name and amount before confirming. That habit matters in crowded markets and restaurants where several QR codes may be visible. Screenshotting receipts can help if a vendor asks for proof.

PromptPay, Cards And Cash

PromptPay has not made cash irrelevant. Many Bangkok venues accept cards and QR. Some local stalls prefer QR or cash. Some tourist-facing businesses still push cards. Upcountry, islands and small transport operators can be less predictable. The best setup is mixed: local mobile banking if you have it, a no-drama card, and enough cash for the day.

For expats, PromptPay is worth learning early because it affects rent transfers, splitting bills, paying small vendors and receiving money from Thai contacts. For tourists, it is worth understanding so you know why locals pay differently and why a stall may ask for bank transfer rather than card.

FAQ

Is PromptPay the same as a credit card?

No. PromptPay is payment and transfer infrastructure linked to bank accounts and participating providers, not a credit-card network.

Can tourists use PromptPay without a Thai bank account? Usually not in the same way locals do. Short-stay visitors should expect to use cash, cards or travel payment products unless they have local banking access.

Are small PromptPay transfers free? BOT’s standard table lists transfers up to THB 5,000 as free, and notes that most banks have waived fees for digital payment transactions since 2018.

The safe approach is to treat PromptPay as part of Thailand’s financial plumbing. It is extremely useful once you are inside the local banking system, but it does not remove the need for payment backups. Check your bank’s current terms before making large transfers or relying on it for business payments.

{kind=link}